The EU Carbon Border Adjustment Mechanism (CBAM) is changing how industrial exports enter Europe. For Saudi Arabia, the cbam impact saudi arabia is not only about new paperwork. It is also about competitiveness and new carbon-linked costs. CBAM links climate rules to trade, with the stated goal of preventing “carbon leakage.” This matters most for energy-intensive products that face high scrutiny in Europe.

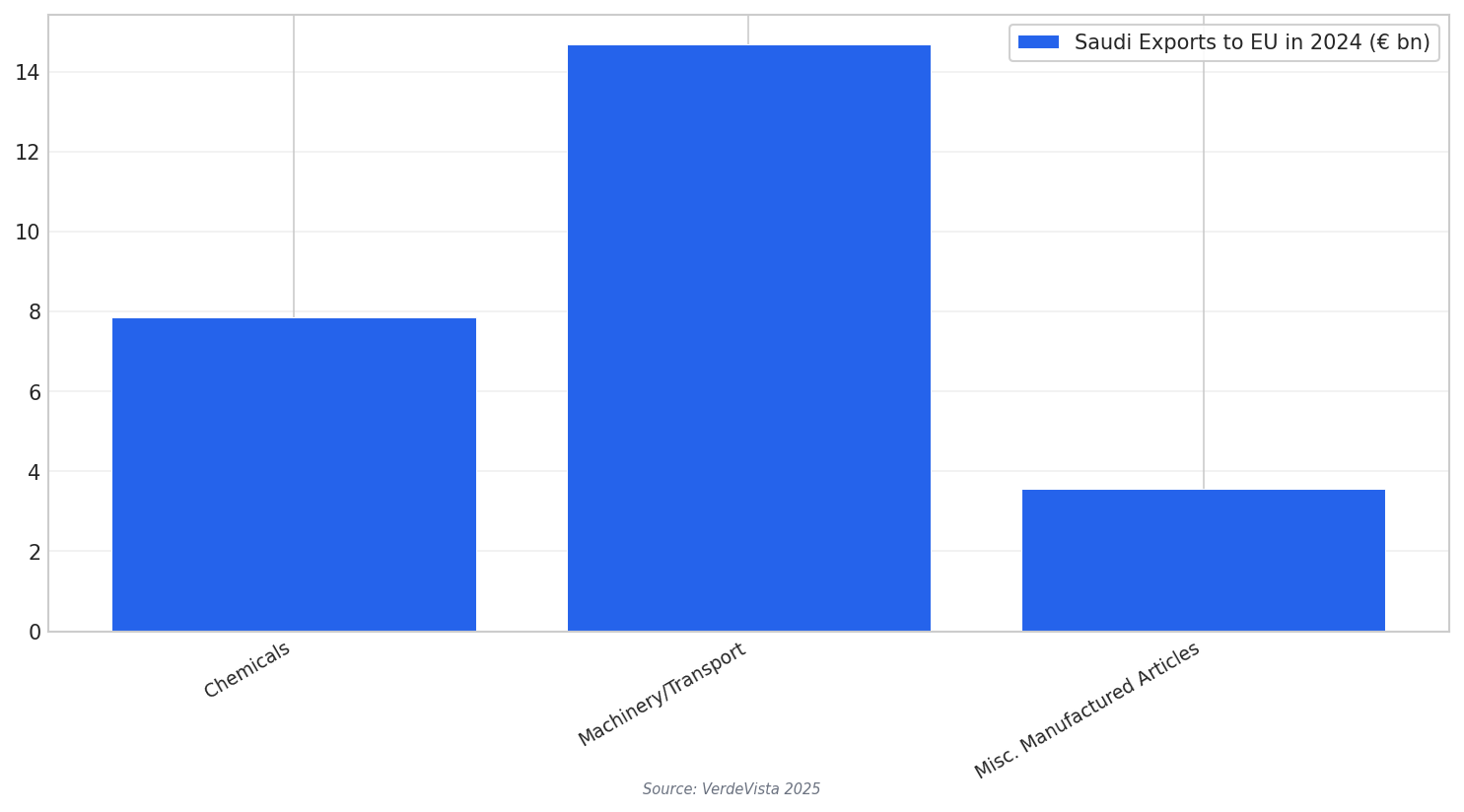

Saudi–EU trade is large, so small rule changes can create big pressure. In 2024, total bilateral goods trade reached about €69.9 billion. Imports from Saudi to the EU were €33.07 billion, while exports from the EU to Saudi were €36.84 billion. Saudi exports to the EU grew 7.5% year-on-year from 2023 to 2024, while imports from the EU dropped 9.5%. Chemicals were a major Saudi export category at €7.86 billion, or 21%.

Major Saudi export categories to the EU also included Machinery/Transport at €14.7 billion (40%) and Misc. Manufactured Articles at €3.57 billion (10%). These figures show how much is at stake if CBAM creates new costs or slows shipments through reporting errors.

CBAM was implemented in two phases. In the transitional phase, from 1 October 2023 to 31 December 2025, importers had to report emissions, but no charges applied. In the definitive phase, starting on 1 January 2026, financial obligations begin and will be rolled out over a nine-year period. Importers must purchase and surrender CBAM certificates linked to the greenhouse gas emissions embedded in covered goods.

Why Costs and Verification Now Decide EU Market Access

A key risk for Saudi exporters is the carbon cost signal coming with 2026. One Arab-region assessment estimates carbon costs of 70 to 95 Euros per ton of CO₂ emitted under the EU Emissions Trading System (ETS). The same assessment warns that if regional industries do not implement domestic decarbonization reforms and mitigation efforts, competitiveness in the European market will dwindle. In practice, CBAM can behave like a trade barrier if firms cannot prove low embedded emissions.

This hits petrochemical-linked value chains and also metals and building materials. Saudi exporters in industrial sectors such as petrochemicals, metals, and cement are pushed to measure and document emissions. During the transitional phase, EU importers must submit quarterly CBAM reports covering quantities imported, embedded direct and indirect emissions, and any carbon pricing applied in the country of origin. VerdeVista notes that non-compliance can affect market access, impose penalties, or trigger import restrictions.

For aluminum and cement exporters, the practical challenge is data quality, not only production. Reported hurdles include complex carbon footprint measurement for Scope 1 and 2 emissions, and the need for emissions data to be verified under EU-recognised standards such as ISO 14064-3 and ISO 17029. Across the Arab region, CBAM is also pushing interest in Monitoring, Reporting, and Verification (MRV) systems, and in defensive policy options like carbon pricing mechanisms and even domestic ETSs.

When does CBAM move from reporting to paying charges?

What is the estimated carbon cost range mentioned for Arab-region exports to the EU?

What does cbam impact saudi arabia mean for exporters in practice?

What must EU importers report under the CBAM transitional phase?

Talk to us for your needs in:

-

Energy Efficiency Strategy & Feasibility

-

Renewable Energy Strategy & Investment Advisory

-

Digital Energy & Smart Grid Strategy

-

Market Entry Strategy

-

Sustainability & Impact Strategy

-

Energy Project Governance & PMO Advisory

-

Energy Market Research

-

Energy Stakeholder & Customer Research

-

Energy Market Intelligence

-

Energy Feasibility & Investment Assessment

-

Energy Sector Benchmarking & Performance Strategy