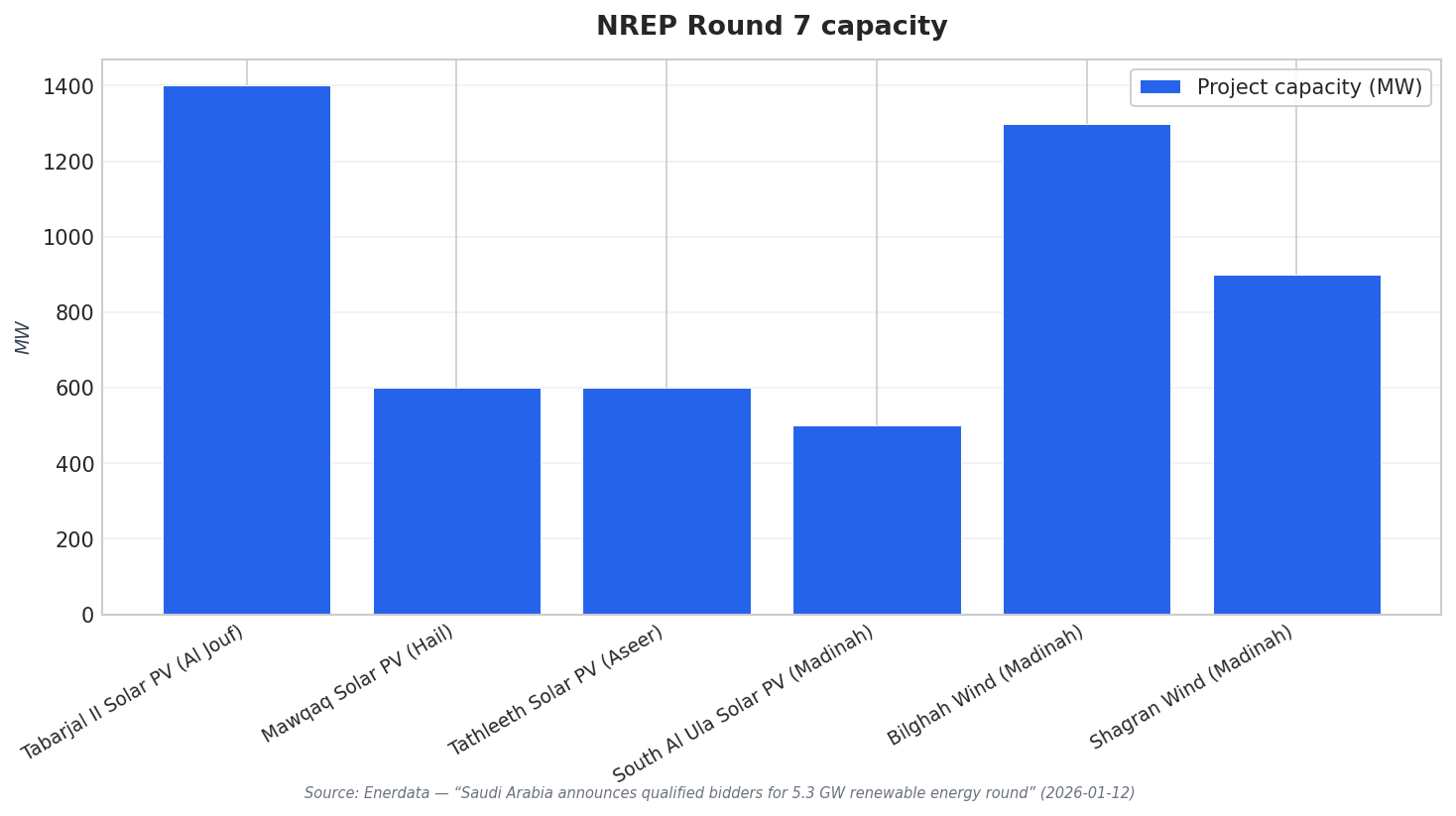

Tabarjal II is positioned as one of the biggest individual assets inside Saudi Arabia’s National Renewable Energy Program (NREP) Round 7. In the official Round 7 package managed by the Saudi Power Procurement Company (SPPC), Tabarjal II Solar PV IPP is listed at 1.4 GW and is located in Al Jouf. The same round totals 5.3 GW across solar PV and wind. Solar projects include Tabarjal II (1.4 GW), Mawqaq (600 MW) in Hail, Tathleeth (600 MW) in Aseer, and South Al Ula (500 MW) in the Madinah region. The wind portfolio adds 2.2 GW through Bilghah (1.3 GW) and Shagran (900 MW), both in the Madinah region.

That pipeline matters because SPPC’s qualified bidder list shows a deep field that can move quickly once procurement advances. For solar PV IPPs, qualified companies include Masdar, EDF Power Solutions, Engie, Sembcorp Utilities, Jinko Power (HK), TotalEnergies Renewables, Korea Electric Power Corporation (KEPCO), SPIC Shanghai Electric Power Company, and local developers. SolarQuarter also lists additional qualified names across managing and technical roles, including Alfanar, Al Gihaz Holding Company, Al Jomaih Energy & Water Company, Nesma Renewable Energy, Korea Western Power Company, Marubeni Corporation, and others. This breadth suggests that the tabarjal solar project saudi arabia story is not only about one site, but also about the scale and competitiveness of the auction environment shaping 2026 execution.

Where 2026 Momentum Comes From: Equipment, Structures, and Local Content

Behind the project headlines, Saudi Arabia’s 2026 buildout is tied to equipment availability and balance-of-system readiness. IndexBox projects the Saudi Arabia solar equipment market at about USD 3.5–4.5 billion in 2026, rising to USD 10–14 billion by 2035. In the same 2026 context, module prices are cited at about USD 0.08–0.12 per watt-peak (Wp) for mainstream PERC and TOPCon bifacial panels, while full EPC turnkey costs for utility-scale projects range from USD 0.45–0.65 per watt (AC). IndexBox also notes that local content requirements under the “Made in Saudi” program are pushing international suppliers toward in-Kingdom module assembly, inverter manufacturing, and mounting fabrication, with facilities announced or under construction in 2025–2026.

Mounting and tracking choices are another lever that can affect speed and standardization across large projects like Tabarjal II. IndexBox estimates the Saudi Arabia solar panel mounting structure market at about USD 180–220 million in 2026, reaching around USD 450–550 million by 2035. Single-axis trackers account for over 65% of utility-scale installations, supported by a 15–25% energy yield premium over fixed-tilt systems. In 2026, mounting structure system prices are described at USD 0.08–0.14 per watt DC for fixed-tilt ground mount and USD 0.12–0.20 per watt DC for single-axis trackers. IndexBox also estimates imports satisfy roughly 55–65% of total volume in 2026, while new fabrication lines with robotic welding came online in Dammam and Jubail in 2024–2025.

Saudi Arabia’s broader market signals reinforce why Round 7 projects can be framed as part of a 2026 sprint. Mordor Intelligence estimates the Saudi Arabia solar energy market size in 2026 at 13.47 GW, up from 10.25 GW in 2025, and projects 52.72 GW by 2031, implying 31.40% CAGR over 2026–2031. Separately, Mordor Intelligence notes a USD 1.2 billion joint venture between JinkoSolar and the Public Investment Fund to establish a 10 GW solar cell and module manufacturing facility in Riyadh, with production scheduled to commence in 2026. Taken together with SPPC’s 5.3 GW Round 7 slate, Tabarjal II in Al Jouf becomes a concrete anchor point for how capacity awards, supply chains, and localization pressures intersect in 2026.

What is Tabarjal II and where is it located?

How much capacity is included in Saudi Arabia’s NREP Round 7 package?

Which other solar projects sit alongside Tabarjal II in Round 7?

What do 2026 market forecasts say about Saudi Arabia’s solar equipment scale-up?

Why do mounting structures and trackers matter for the Tabarjal solar project in Saudi Arabia?

Talk to us for your needs in:

-

Energy Efficiency Consulting

-

Renewable Energy Integration

-

Smart Grid Solutions

-

Market Entry Strategy

-

Sustainability Assessment

-

Project Management Excellence

-

Energy Market Research

-

In-Depth Market Survey for Energy

-

Market Intelligence and Insights in Energy

-

Feasibility Study and Assessment in Energy

-

Saudi Energy Benchmarking