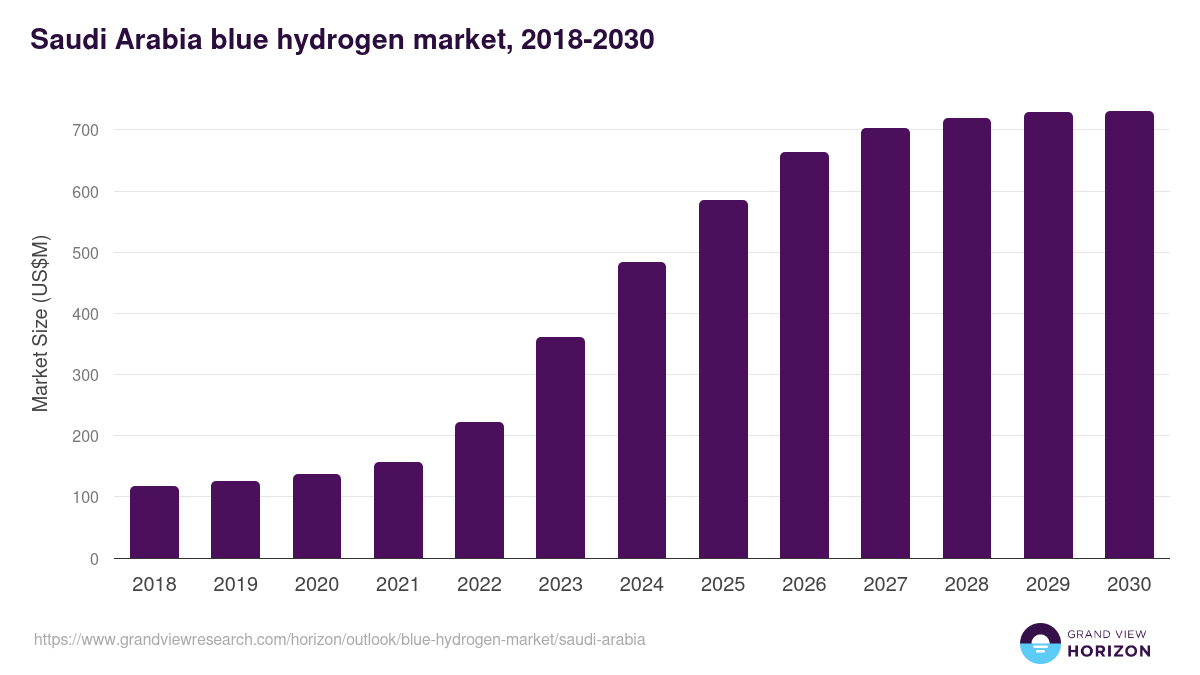

Aramco’s 11 million-tonne blue ammonia target by 2030 shows how serious the company is about long-term exports to Asia. The push aligns with Saudi Arabia’s growing role in the Saudi Blue Hydrogen market, which reached USD 483.4 million in 2024 and is projected to hit USD 730.3 million by 2030. The global market is also rising, growing from 4.11 million tons in 2025 to 5.91 million tons in 2030. This gives Saudi Arabia a clear opening to secure a large share.

Saudi Blue Hydrogen Market: Why Japan and Korea Drive the Blue Shift

Aramco’s recent moves toward Japan and South Korea explain the speed behind the 2025 pivot. A 40-ton blue ammonia shipment to Japan in 2020 and 25,000 tons to South Korea in 2022 proved that export routes work. Japan’s INPEX projects and Korea’s clean hydrogen plans make them ideal partners. For Aramco, these markets provide steady demand and long-term energy security. For the Saudi Blue Hydrogen market, they validate the country’s plans to capture 15% of global blue hydrogen output by 2030.

Read Also: Inside Saudi Arabia’s Renewable Hydrogen Push: The Future of Green Energy Export

Grid Bottlenecks That Slow the Transition

Saudi Arabia wants to add 120 GW of generation capacity by 2032. Today the system produces 55 GW, and rising demand strains the grid. Transmission losses are high, and renewables are not fully integrated. To fix this, the Ministry and the Saudi Power Procurement Company (SPPC) launched major tenders.

The most important is the 2 GW / 8 GWh battery storage tender from late 2024, with prequalified bidders announced in January 2025. Additional 4 GWh storage deals were awarded in 2025. These projects target Makkah, Qassim, and Hail under a build-own-operate model. Such upgrades show where the system is weakest: storage, transmission stability, and renewable integration.

Read Also: Acwa Power’s Saudi Renewable Projects Reach 34 GW

New Power Projects Show Expansion Pressure

The country is adding supply fast. New tenders include 3.1 GW of solar and 2.2 GW of wind projects, with bids due in September 2025.

Another tender for 6 GW of CCS-ready CCGT plants is planned for 2025 to support hydrogen integration. A separate July 2025 tender seeks electrical reserve storage for government buildings. These numbers point to a common issue: demand is rising faster than the grid can evolve.

Regulation Pressures Heavy Industry, Not Only for the Saudi Blue Hydrogen Market

A major shift came with new emission penalties introduced in late 2025. These penalties push industries toward CCUS, helping expand a market worth USD 68.9 million in 2025 and projected to reach USD 146 million by 2032. The Ministry’s long-term plan targets 44 million tons of annual CO₂ storage by 2035.

A key part of this effort is the Jubail CCS hub, which will capture 9 million tons yearly from Aramco’s gas plants starting in 2027. Saudi Arabia’s 2025-2030 Industrial Decarbonisation Strategy adds urgency, committing $187 billion to cutting 20 million tons of emissions each year.

A System Under Pressure, Ready to Change

Saudi Arabia’s energy system is being rebuilt while blue hydrogen takes center stage. Aramco’s export strategy, massive grid tenders, and new emission rules show a country pushing toward a lower-carbon future while handling real limits in infrastructure. The Saudi Blue Hydrogen market stands at the center of this shift. To understand how your organization can navigate these rapid changes, consider reaching out to Eurogroup Consulting, a global firm supporting energy transformation across complex markets.

Talk to us for your needs in:

-

Energy Efficiency Strategy & Feasibility

-

Renewable Energy Strategy & Investment Advisory

-

Digital Energy & Smart Grid Strategy

-

Market Entry Strategy

-

Sustainability & Impact Strategy

-

Energy Project Governance & PMO Advisory

-

Energy Market Research

-

Energy Stakeholder & Customer Research

-

Energy Market Intelligence

-

Energy Feasibility & Investment Assessment

-

Energy Sector Benchmarking & Performance Strategy